Guide

French Inheritance Tax Explained: A Guide for UK Families

Confused about French inheritance tax? Our plain-English guide explains who pays the tax, available allowances, tax rates, deductible debts, double taxation between the UK and France, and the role of the French notary in calculating and declaring inheritance tax during a French succession.

One of the biggest concerns for UK families inheriting assets in France is understanding French inheritance tax.

Many people assume it works like UK Inheritance Tax. In reality, the two systems are very different.

In France, inheritance tax is generally paid by each beneficiary, not by the estate as a whole. The amount each person pays depends on their relationship to the deceased, the value of what they inherit and the tax allowances available to them.

Understanding these rules early can help you prepare for the succession and avoid unexpected surprises.

Is French Inheritance Tax Always Payable?

Not necessarily.

Whether French inheritance tax is payable depends on several factors, including:

- Where the deceased was domiciled.

- Where the assets are located.

- The value of the inheritance.

- The relationship between the deceased and each beneficiary.

- Whether any exemptions or international tax treaties apply.

If the deceased owned property in France, French inheritance tax is commonly relevant, even where the beneficiaries live in the UK.

Who Pays the Tax?

Unlike the UK system, where inheritance tax is usually settled from the estate before beneficiaries receive their inheritance, French inheritance tax is generally assessed individually.

Each beneficiary receives their own tax calculation based on:

- The value of the assets they inherit.

- Their personal tax allowance.

- Their relationship to the deceased.

- The applicable tax bands.

This means two beneficiaries inheriting different amounts may pay different amounts of tax.

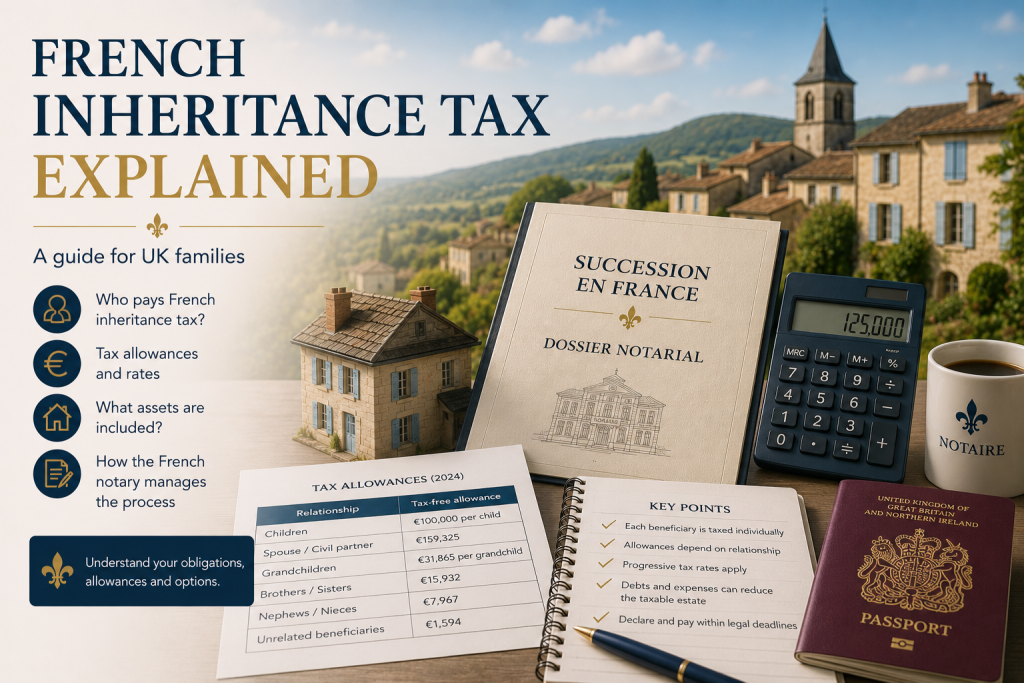

Tax Allowances

French inheritance tax provides allowances before tax becomes payable.

The amount depends on the relationship between the deceased and the beneficiary.

For example:

- Children generally receive one of the largest tax-free allowances.

- Surviving spouses and civil partners are generally exempt from French inheritance tax.

- More distant relatives receive much smaller allowances.

- Unrelated beneficiaries often receive very limited allowances and significantly higher tax rates.

These allowances are reviewed by the French government from time to time, so your notary will calculate the current figures applicable to your succession.

Tax Rates

After deducting any available allowance, French inheritance tax is charged using progressive tax bands.

The closer your relationship to the deceased, the more favourable the tax rates generally are.

Children usually benefit from the lowest rates, while distant relatives and unrelated beneficiaries can face substantially higher taxation.

For this reason, obtaining accurate property valuations and ensuring all deductible liabilities are included can make a significant difference to the final tax calculation.

What Assets Are Included?

The estate may include:

- French property.

- UK property.

- French bank accounts.

- UK bank accounts.

- Investments.

- Vehicles.

- Business interests.

- Valuable personal possessions.

- Certain trust interests.

- Other worldwide assets, depending on the circumstances.

Exactly which assets are taxable in France depends on the facts of the succession and the applicable laws.

Debts Can Reduce the Taxable Estate

Not every asset value is taxed without adjustment.

Certain liabilities may reduce the taxable value of the estate, including:

- Mortgages.

- Outstanding loans.

- Funeral expenses (subject to French rules).

- Certain unpaid taxes.

- Other legally deductible debts existing at the date of death.

Your French notary will advise which liabilities can be deducted when preparing the inheritance tax declaration.

What About Gifts Made During Lifetime?

France has detailed rules covering gifts made before death.

Previous gifts made by the deceased can affect:

- Available tax allowances.

- The inheritance tax calculation.

- The distribution of the estate.

Your notary will usually ask whether the deceased made gifts to any beneficiaries during their lifetime and may request supporting documentation.

This is one reason why keeping records of gifts is so important.

When Is the Tax Paid?

The inheritance tax declaration is normally prepared by the French notary.

Payment deadlines depend on the circumstances of the succession, but French law generally requires inheritance tax to be declared and paid within specific statutory time limits.

Missing these deadlines can result in interest and financial penalties.

If delays occur because documents are difficult to obtain—particularly in international estates—it is still important to keep your notary informed so the succession can progress as quickly as possible.

Will I Pay Tax Twice?

This is one of the most common questions UK families ask.

The UK and France have agreements designed to reduce the risk of the same assets being taxed twice.

Exactly how these rules apply depends on:

- The deceased’s domicile.

- Where assets are situated.

- The type of asset.

- The taxes already paid in each country.

International successions can be complex, and specialist advice is often required where both UK and French tax systems are involved.

What Does the French Notary Do?

The French notary plays a central role in the inheritance tax process.

They will typically:

- Identify the heirs.

- Value the estate.

- Calculate each beneficiary’s inheritance.

- Prepare the inheritance tax declaration.

- Calculate the tax due from each beneficiary.

- Submit the declaration to the French tax authorities.

- Arrange payment before finalising the succession.

Because the notary is responsible for ensuring the declaration is legally correct, they may request a significant amount of supporting documentation before they can complete their calculations.

Practical Tips

A few simple steps can make the process much smoother:

- Keep copies of all bank statements and valuations.

- Tell your notary about any lifetime gifts.

- Respond promptly to requests for documents.

- Retain invoices for deductible expenses.

- Ask questions if you do not understand how the tax has been calculated.

- Keep copies of everything you submit.

Final Thoughts

French inheritance tax often seems intimidating at first, particularly for UK families unfamiliar with the French legal system.

However, once you understand that the tax is calculated separately for each beneficiary—and that allowances, family relationships and deductible debts all play an important role—the process becomes much easier to follow.

Your French notary will calculate the tax due and prepare the necessary declarations, but staying organised and understanding the basics will help you navigate the process with greater confidence.