Guide

What Happens to Pensions After a Death?

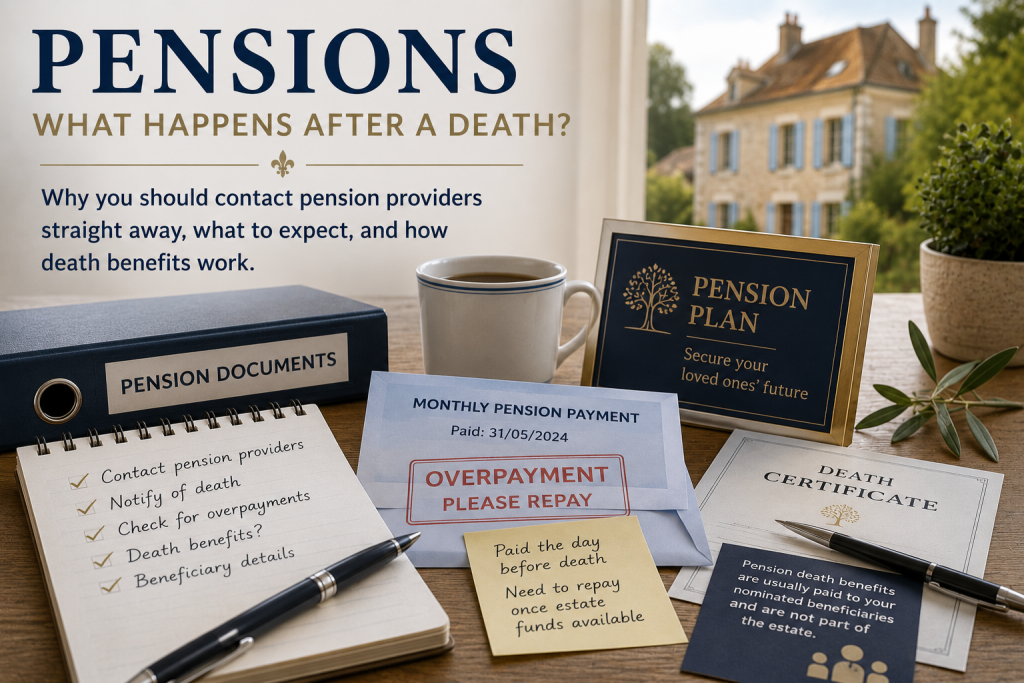

Pensions are often overlooked during a French succession, yet they can create unexpected challenges. This guide explains why you should contact pension providers quickly, what happens if a payment is made after death, and why pension death benefits are usually separate from the estate itself.

When someone dies, it’s important to notify any pension providers as soon as reasonably possible.

Many pensions continue to pay monthly, and if a payment is made after the member’s death, the provider may ask for it to be returned.

This can become particularly difficult if the deceased’s bank accounts have already been frozen.

Contact Pension Providers Promptly

As soon as you’ve obtained the relevant details, contact each pension provider and inform them of the death.

They will usually ask for:

- The deceased’s full name.

- Date of birth.

- Date of death.

- Policy or membership number (if known).

- A copy of the death certificate.

It’s helpful to keep a record of who you spoke to and any reference numbers they provide.

Payments Made After Death

One situation that often catches families by surprise is when a pension payment is made shortly after the person’s death.

In our own case, my father died just before his monthly pension payment was due.

The payment was made as normal, but once the pension provider became aware of the death, they requested that the money be repaid.

Unfortunately, because the bank accounts had already been frozen as part of the succession, accessing the funds to repay them wasn’t straightforward.

If you find yourself in a similar situation, don’t panic.

Explain the circumstances to the pension provider.

In many cases, they’re willing to wait until:

- The French succession has progressed sufficiently for funds to become available; or

- A UK Grant of Probate has been issued, allowing access to the estate.

Clear communication early on can prevent unnecessary stress and avoid formal recovery action while the estate is being administered.

Don’t Assume There Will Be a Death Benefit

Many people expect every pension to pay a lump sum when the member dies.

Unfortunately, that isn’t always the case.

Some pension schemes only provide death benefits if death occurs before retirement or within a specified period after retirement.

In our family’s case, no lump sum was payable because my father had been retired for more than five years, which was beyond the scheme’s qualifying period.

Every pension scheme has its own rules.

The only way to know for certain is to contact the provider directly and ask.

Ask These Questions

When speaking to the pension provider, consider asking:

- Has the pension now been stopped?

- Has any payment been made after death?

- Does that payment need to be repaid?

- Is there a lump-sum death benefit?

- Is there a surviving spouse’s or dependant’s pension?

- Who has been nominated as the beneficiary?

- What documents are required?

- Is there a claim form that needs to be completed?

Writing these answers down will make later stages much easier.

Pension Death Benefits Are Usually Separate from the Estate

One point that often surprises families is that pension death benefits are generally not part of the deceased’s estate.

Instead, they are usually paid directly by the pension trustees or provider to the nominated beneficiary (or beneficiaries), subject to the scheme’s rules.

This means that, in many cases:

- The payment does not form part of the succession.

- It is not distributed according to the deceased’s will.

- It is generally not affected by French forced heirship rules.

The pension provider will normally decide who receives the benefit based on the member’s nomination and the scheme’s governing rules.

If no valid nomination exists, the provider or trustees will usually determine who should receive the benefit in accordance with those rules.

Because every pension scheme is different, always ask the provider how death benefits are handled in your specific circumstances.

Check for More Than One Pension

It’s common for people to have several pensions accumulated over the course of their working life.

Don’t stop after contacting the first provider.

Look for clues such as:

- Annual pension statements.

- Old employer correspondence.

- Bank statements showing pension payments.

- Tax documents.

- Personal paperwork.

If you’re unsure whether other pensions exist, the UK Government’s Pension Tracing Service may also be able to help locate lost or forgotten workplace and personal pensions.

Keep Your Notaire and UK Solicitor Informed

Although pension death benefits are often separate from the estate, regular pension payments, overpayments and related correspondence may still be relevant to the administration of the succession.

Provide copies of any important letters to your notaire or UK solicitor so they have a complete picture of the deceased’s financial affairs.

Final Thoughts

Pensions are one of the few financial arrangements that frequently sit outside both the will and the succession.

That makes them easy to overlook, but they can also provide valuable financial support to beneficiaries or, in some cases, create unexpected issues if payments continue after death.

Notify pension providers promptly, ask whether any death benefits are payable, and don’t assume that the rules for one pension will apply to another. Taking a little time to understand each scheme can save considerable confusion later.